🏦 Difference Between Floating & Fixed Home Loan Rates

When applying for a home loan, one of the most important decisions is whether to choose a fixed interest rate or a floating interest rate. Both have their advantages and limitations, and the right choice depends on your financial goals.

Mettro Housing And Finance

9/12/20251 min read

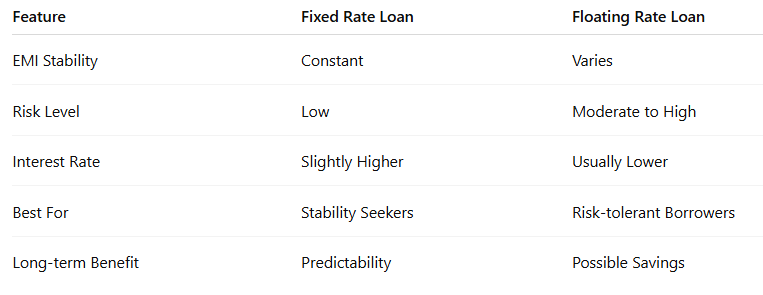

✅ 1. Fixed Interest Rate

The interest rate remains the same throughout the loan tenure.

Your EMI does not change, regardless of market fluctuations.

Provides stability and predictability for long-term financial planning.

Suitable for: Buyers who prefer certainty and don’t want surprises in EMIs.

🔸 Example: If your fixed home loan rate is 9%, you’ll pay the same interest for the full loan period even if market rates drop or rise.

✅ 2. Floating Interest Rate

The interest rate changes with market conditions (linked to RBI repo rate or lender’s benchmark).

EMIs may increase or decrease during the loan tenure.

Usually cheaper than fixed rates in the long run.

Suitable for: Buyers who are comfortable with some risk and fluctuations.

🔸 Example: If your floating home loan starts at 8.5%, it may reduce to 7.9% when rates fall, or rise to 9.2% if rates increase.

🔍 Key Differences at a Glance

💡 Expert Advice

If you value peace of mind and stable EMIs, go with a fixed rate.

If you can manage fluctuations and want to save in the long run, choose a floating rate.

Some banks also offer hybrid loans — fixed for the first few years, then floating later.

Address

Shop no 8 Agarwal lifestyle Global city virar west Virar, India 401303 Maharashtra

Contacts

+91 70208 37164

mak.juhi@gmail.com